Are you juggling multiple debts and struggling to keep track of payments? Managing several loans can feel overwhelming and costly, but what if there was a way to simplify your finances and potentially save money?

A Loan Consolidation Planning Tool is designed just for you—to help combine your debts into one manageable payment. Imagine reducing stress and gaining control over your money with a clear plan tailored to your situation. Keep reading to discover how this tool works and how it can transform your path to financial freedom.

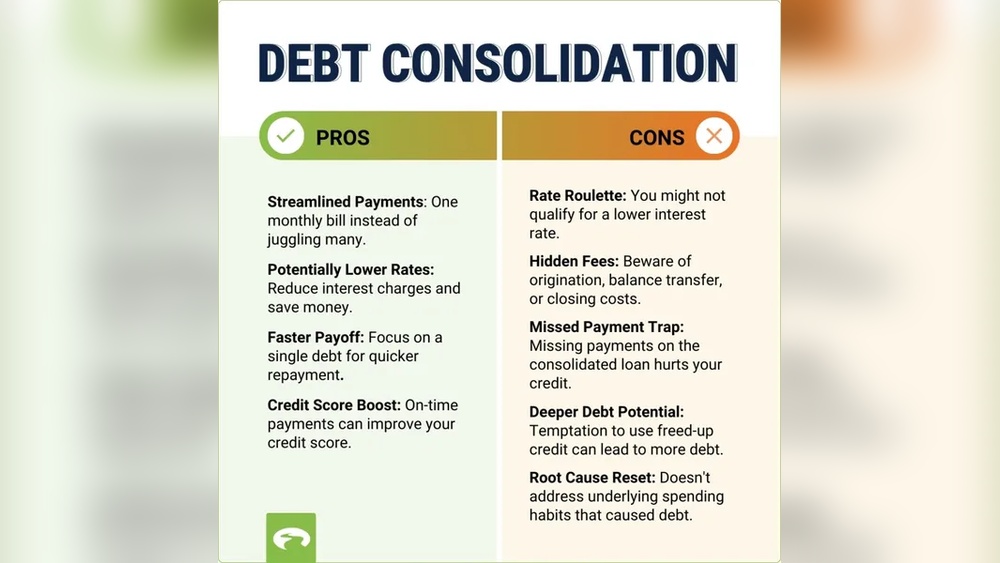

Benefits Of Loan Consolidation

Lower interest rates help save money on overall debt costs. Consolidating loans often means getting a loan with a smaller interest rate. This reduces the amount paid each month. It can also lower the total amount paid over time.

Simplified payments make managing money easier. Instead of many due dates and amounts, there is only one payment per month. This helps avoid missed payments and late fees. It reduces stress and confusion.

Improved credit score may happen with loan consolidation. Making on-time payments on one loan shows good financial habits. It can increase credit scores over time. Better credit scores can lead to better loan offers later.

Faster debt repayment is possible by lowering interest and focusing on one payment. More money goes toward the principal balance. This helps pay off debt quicker and frees up money for other needs.

How Loan Consolidation Works

Loan consolidation combines several loans into one. This helps simplify payments and may lower interest rates. Common types include federal student loan consolidation and private loan consolidation. Federal consolidation combines government student loans. Private consolidation uses a new loan from a bank or lender.

Eligibility depends on loan type and credit score. Federal loans usually need to be in repayment or grace period. Private loans often require good credit and income proof.

The application process starts by gathering loan details. Then, submit the application online or in person. For federal loans, use the official government website. Private lenders have their own forms and checks. Approval time varies but usually takes a few weeks.

Choosing The Right Planning Tool

Choosing the right loan consolidation tool helps simplify debt management. Key features include easy input fields for debts, clear payment breakdowns, and interest rate comparisons. Tools should offer accurate results and be user-friendly.

Top online calculators from banks like Wells Fargo, U.S. Bank, PNC, and Navy Federal provide reliable estimates. They show how much you can save and your new monthly payments. These calculators often allow you to enter credit card balances and loan amounts.

Mobile apps are handy for tracking consolidation plans on the go. Look for apps with simple interfaces and real-time updates. They help you stay on top of your debt payments and progress.

Using A Loan Consolidation Planning Tool

Start by entering the total amount of your debts. Include credit cards, personal loans, and other loans. Make sure the numbers are accurate for the best results.

The tool will show your estimated monthly payments based on the data you provide. This helps you see how much you might pay each month with a consolidation loan.

Compare different loan options side by side. Look at the interest rates, loan terms, and monthly payments. This makes it easier to find the best deal for your needs.

Common Mistakes To Avoid

Ignoring fees and penalties can increase your loan cost a lot. Some lenders charge early repayment fees or other hidden costs. Always check the fine print before you agree to consolidate your loans.

Overlooking loan terms might lead to surprises. The interest rate or repayment period could be different from your original loans. Make sure to compare all terms carefully to avoid paying more in the long run.

Failing to budget properly is a common mistake. Monthly payments might change after consolidation. Create a clear budget to include your new payment and avoid missed payments or extra debt.

Alternatives To Loan Consolidation

The Debt Snowball Method focuses on paying off the smallest debts first. You pay minimums on all debts, except the smallest one. Extra money goes to that debt until it is paid off. This builds motivation as debts disappear one by one.

Debt Settlement means negotiating with lenders to reduce the total amount owed. It can lower your balance but may hurt your credit score. Settlements often require a lump-sum payment or a payment plan.

Credit Counseling Services offer help from professionals. They create a budget and plan to manage your debt. Counselors may also set up a debt management plan with lower interest rates and single monthly payments.

Tips For Maximizing Savings

Negotiating lower interest rates can reduce your monthly payments. Contact lenders and ask for better terms. Explain your good payment history and credit score. Even a small rate cut saves money over time.

Setting up automatic payments helps avoid late fees. It keeps your credit score healthy. You save time and stress by not missing payments. Many lenders offer small discounts for autopay.

Maintaining financial discipline is key to success. Stick to your budget and avoid new debt. Track your spending and save extra money to pay off loans faster. Consistency leads to long-term savings and peace of mind.

Local Options In Austin, Texas

Banks in Austin offer various consolidation loans to help manage debt. They provide fixed interest rates and flexible payment plans. Examples include Wells Fargo, U.S. Bank, and PNC Bank. These banks often provide online calculators to estimate payments easily.

Credit unions are great local options with lower fees and personalized service. Austin-area credit unions like Amplify Credit Union and Austin Telco offer consolidation loans. They focus on community support and better interest rates than big banks.

Many community resources in Austin provide free financial education. Nonprofits and local workshops teach budgeting and debt management skills. These resources help plan loan consolidation wisely.

Financial advisors near you can give tailored advice. They review your debts, income, and goals to create a clear plan. Advisors in Austin can help find the best loan options and improve your credit score.

Frequently Asked Questions

Why Does Dave Ramsey Not Recommend Debt Consolidation?

Dave Ramsey discourages debt consolidation because it can extend debt repayment, increase total interest, and delay financial freedom. He promotes a debt snowball method instead.

How Much Is The Payment On A $50,000 Consolidation Loan?

Monthly payments on a $50,000 consolidation loan depend on interest rates and loan terms. Typically, payments range from $900 to $1,200 for a 5-year term at 6% to 8% interest. Use a loan calculator for precise estimates based on your specific rate and duration.

Does Huntington Offer Debt Consolidation?

Huntington offers unsecured personal loans that you can use to consolidate high-interest debt into one payment.

How To Pay Off $30,000 In Debt In 1 Year?

Create a strict budget, increase income, and cut expenses. Prioritize high-interest debts first. Consider debt consolidation or refinancing to lower interest rates. Make extra payments monthly and track progress. Stay disciplined to fully repay $30,000 in one year.

Conclusion

Using a loan consolidation planning tool simplifies your debt management process. It helps you see your total debt clearly and plan payments better. You can find options that fit your budget and save money on interest. This tool supports smarter financial choices and reduces stress.

Take time to explore different scenarios before deciding. A well-planned consolidation can improve your credit and financial health. Start with accurate information and stay committed to your plan. Your path to easier debt repayment begins with thoughtful planning.